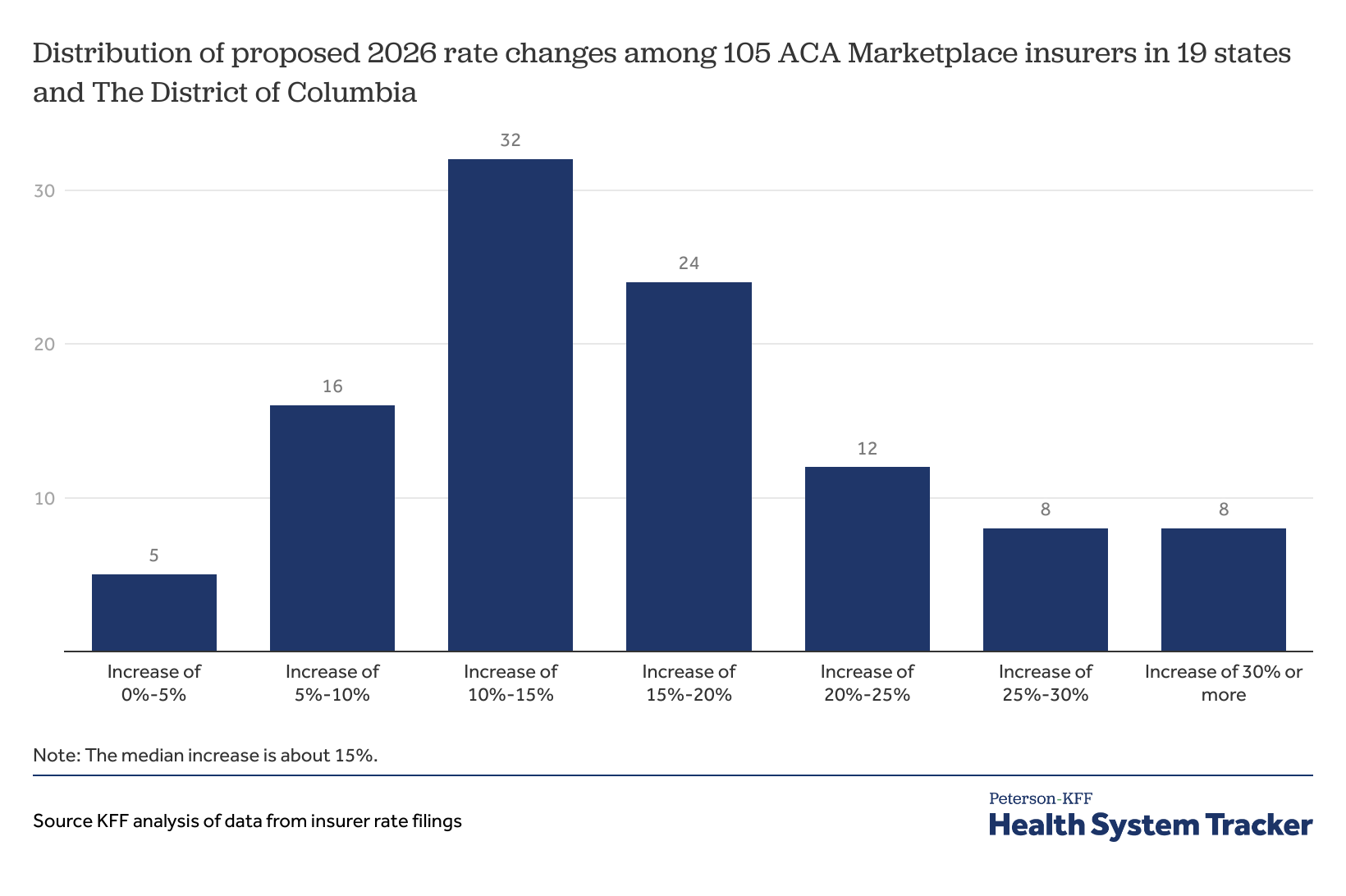

The Affordable Care Act (ACA) marketplace is bracing for its most significant premium spike since 2018, with insurers proposing median increases of 15% for 2026 coverage. This unprecedented hike threatens to undermine the health law’s affordability gains, particularly as enhanced subsidies expire.

Middle-income families could see their monthly premiums nearly double, creating a coverage crisis for millions. The triple whammy of subsidy rollbacks, medical tariffs, and healthcare inflation is reshaping the insurance landscape—and consumers’ wallets.

- ACA insurers propose median 15% premium hikes for 2026, marking the steepest increase since 2018, with some states requesting over 18% increases.

- Expiration of enhanced subsidies will raise average out-of-pocket costs by 75%, risking healthier enrollees dropping coverage and destabilizing insurance pools.

- New medical import tariffs add ~3% to premiums, compounding with healthcare inflation to create a “double whammy” for consumers.

- Middle-income enrollees face the sharpest subsidy cliff, potentially paying 15%+ of income for silver plans versus 8.5% in 2025.

Why Are ACA Insurance Premiums Skyrocketing in 2026?

The Affordable Care Act (ACA) marketplace is bracing for unprecedented premium hikes in 2026, with insurers proposing median increases of 15% nationwide—the largest jump since 2018. This surge stems from a perfect storm of policy shifts and economic pressures. The expiration of enhanced subsidies enacted during the pandemic will remove critical financial cushions for 13 million Americans, while new tariffs on medical imports add 3-4% to insurers’ costs. Healthcare inflation, currently running at 6.7% annually, compounds these pressures.

Regional disparities reveal deeper challenges: Maryland insurers request 18.7% hikes while Texas averages 14.2%. This variance reflects state-specific regulations and provider market concentration.

The Hidden Math of Risk Pools

Insurer filings show disproportionate impacts:

- Sicker enrollees incur 4-7x higher costs than healthy participants

- Every 1% drop in healthy enrollment triggers 2.3% premium increases

3 Key Drivers Behind the 2026 ACA Cost Surge

Three primary factors converge to create the 2026 premium crisis:

- Subsidy Sunset: Enhanced tax credits will vanish December 31, 2025, exposing enrollees to true plan costs.

- Medical Tariffs: New 15-25% duties on Chinese medical imports affect everything from PPE to MRI components.

- Claims Inflation: Hospital prices rose 8.4% in Q1 2025—double the pre-pandemic average.

Insurer profit margins tell a nuanced story—while publicly traded insurers report 4-6% margins, nonprofit ACA specialists like Bright Health operate at -3% to 1% margins.

How Subsidy Changes Will Impact Your Wallet

The subsidy rollback will hit middle-class families hardest. A 40-year-old earning $55,000 currently pays $330/month for a silver plan—this will spike to $580/month in 2026. The “subsidy cliff” returns at 400% of the Federal Poverty Level ($58,320 for individuals).

| Income | 2025 Premium | 2026 Projected | Increase |

|---|---|---|---|

| $30,000 | $85 | $210 | 147% |

| $55,000 | $330 | $580 | 75% |

State-Level Safety Nets

14 states have created bridge programs:

- Massachusetts: 6-month transitional subsidies

- California: State-funded premium assistance

Short-Term Insurance: A Risky Alternative

As ACA costs rise, short-term plans advertising $150/month prices look tempting—but conceal dangerous gaps:

Key limitations:

- Pre-existing condition exclusions apply

- Lifetime caps as low as $250,000

- Can deny renewal after major claims

Strategic Options for 2026 Enrollment

Smart shoppers can mitigate impacts through:

1. Metal Tier Adjustment

Bronze plans will see smaller percentage increases (averaging 12%) than Gold plans (18%). Deductibles rise accordingly.

2. Narrow Network Plans

HMOs with 50-70% fewer providers offer 15-22% savings over PPOs—verify your doctors participate.

3. Income Optimization

Contributing to HSAs or retirement accounts can lower MAGI—potentially qualifying for greater subsidies.

[figure class=”wp-block-image size-large is-style-default”]

The Political Wildcards That Could Change Everything

Three legislative scenarios could alter 2026 projections:

- Subsidy Extension: Currently stalled in House committees

- Tariff Revisions: Medical device exemptions proposed

- Public Option: 12 states exploring alternatives

Vermont’s pilot program shows promise—state-run plans undercut private insurers by 17% through administrative simplification.

Comments