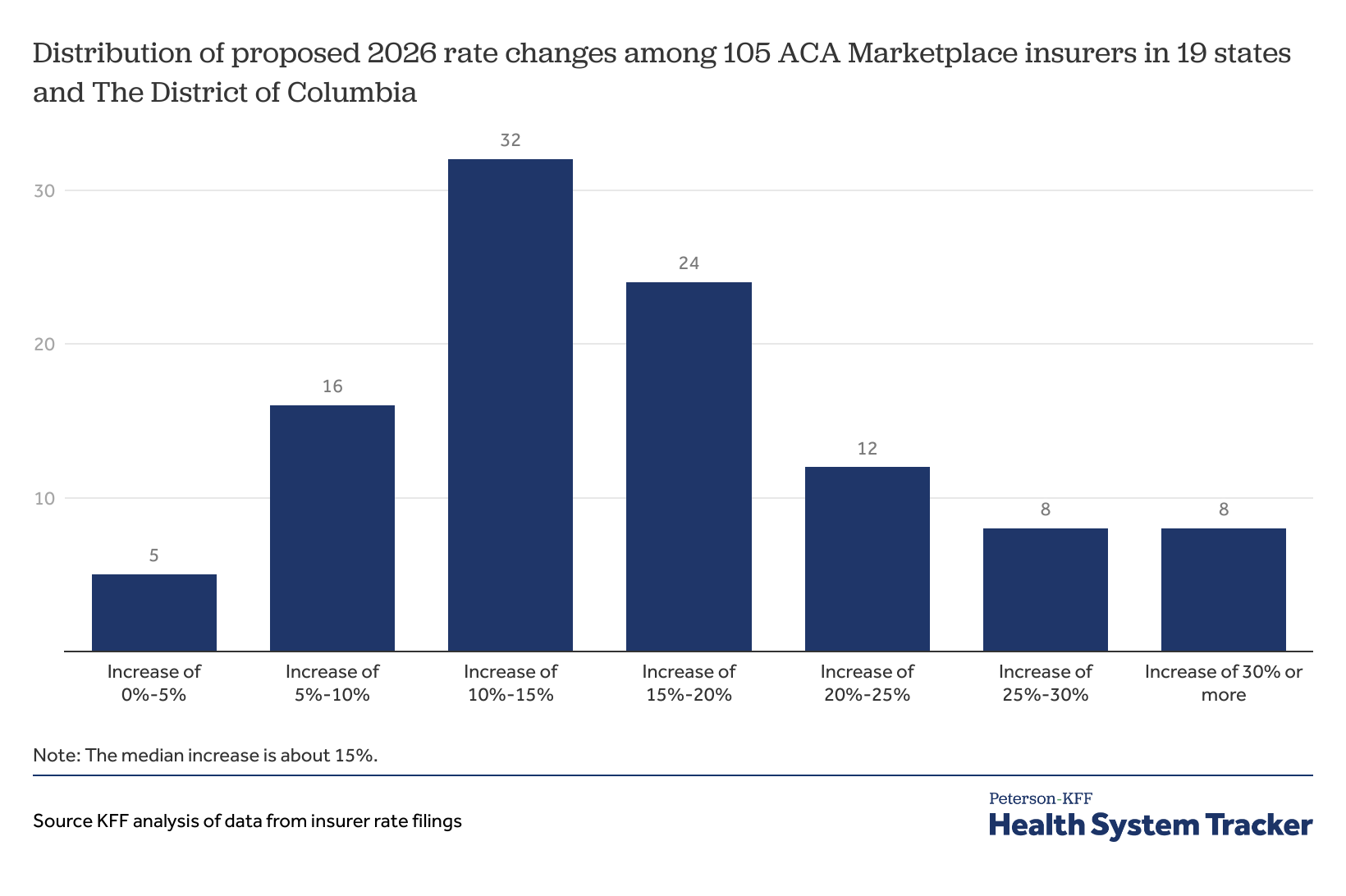

Americans are bracing for the largest ACA premium hike in nearly a decade, with projected increases of up to 75% in 2026. This looming health insurance crisis stems from twin threats: the expiration of pandemic-era subsidies and the ripple effects of Trump administration pharmaceutical tariffs.

Insurers are already proposing median 15% rate increases nationwide, citing rising medical costs and trade policies that could add 3% to drug prices. As subsidies disappear, millions may face impossible choices between coverage and basic necessities.

The Affordable Care Act’s survival isn’t in question—but its affordability is collapsing, threatening to price out the most vulnerable Americans when they need coverage most.

- ACA premiums could surge 75% in 2026 due to expiring pandemic-era subsidies and Trump’s pharmaceutical tariffs, marking the steepest increase since 2018.

- Insurers propose median 15% rate hikes nationwide, driven by subsidy expiration and anticipated 3% cost increases from drug import tariffs.

- A “double whammy” effect may occur as healthier individuals drop coverage, leaving a sicker—and more expensive—risk pool for remaining enrollees.

- Rural residents, chronic illness patients, and subsidized enrollees will be hardest hit by the premium spikes and potential coverage gaps.

- States like Maryland are exploring local subsidies to offset federal cuts, but budget constraints may limit widespread adoption.

The 2026 Health Insurance Crisis: Understanding the 75% ACA Premium Surge

Americans are bracing for the most significant Affordable Care Act (ACA) premium increases since 2018, with projections showing a staggering 75% average rise in 2026. This unprecedented hike stems from the expiration of pandemic-era subsidies and new cost pressures from Trump-era pharmaceutical tariffs. Insurance providers have already filed median 15% rate increase requests nationwide, with some states like Maryland facing proposed jumps up to 18.7%.

The subsidy expiration alone could remove the average 44% monthly discount currently helping 12 million enrollees. Health economists warn this creates a “death spiral” risk—as healthier individuals drop coverage, insurers must raise premiums to cover sicker remaining participants. Rural areas face particular vulnerability, with 35% of counties projected to have just one insurer.

Who Bears the Brunt?

- Subsidy-dependent households: Will see direct 75%+ premium spikes

- Small businesses: Face compounded increases from group plan inflation

- Chronic condition patients: May encounter narrower provider networks as insurers cut costs

Trump’s Tariffs: The Hidden Force Behind Rising Healthcare Costs

While subsidy expiration drives headlines, Trump’s 15-25% tariffs on Chinese pharmaceuticals—including vital generic drugs—are adding ~3% to premium increases. These 2018-era trade policies continue disrupting supply chains, with 72% of key antibiotic ingredients and 45% of generics facing import taxes.

Insurance filings reveal carriers increasingly factoring tariff costs into rates:

| State | Tariff Impact on Premiums | Notable Drugs Affected |

|---|---|---|

| Maryland | 2.8% | Metformin, Lisinopril |

| Colorado | 3.1% | Insulin analogs |

Alternatives When ACA Plans Become Unaffordable

With traditional coverage potentially out of reach for millions, alternatives present risky trade-offs:

- Short-Term Limited Duration (STLD) Plans: 60% cheaper but exclude pre-existing conditions and often cap payouts

- Health Sharing Ministries: Religious-based cost sharing with no coverage guarantees

- State Initiatives: Maryland’s proposed subsidy program could become a national model

Will the ACA Collapse? Separating Hype from Reality

While individual market turmoil grabs attention, the ACA’s Medicaid expansion remains stable—covering 21 million Americans with no premium spikes anticipated. Experts note three stabilizing factors:

- Enhanced subsidies could be reinstated post-election

- States retain authority to implement reinsurance programs

- The individual mandate penalty’s absence reduces political urgency for fixes

The Political Wildcards

2026 premium notices will arrive weeks before midterm elections, creating extraordinary pressure for congressional action. Historical precedents suggest last-minute subsidy extensions are probable—but with potential concessions on drug pricing reforms.

Strategic Moves for Consumers Facing Premium Shock

Proactive measures can mitigate the financial hit:

| Timing | Action | Potential Savings |

|---|---|---|

| Now (2025) | Maximize HSA contributions | $4,150 tax deduction |

| Open Enrollment 2025 | Switch to Bronze HDHP plans | 23% avg premium reduction |

| 2026 Q2 | Lobby state legislators | Possible emergency subsidies |

The coming crisis will test the ACA’s resilience, but history shows American healthcare consistently avoids collapse through messy, last-minute political compromises. As with COVID-era fixes, expect temporary patches rather than systemic reform.

Comments